There were a number of bankruptcy hearings this week, but the big news was Kraken settling charges with the U.S. Securities and Exchange Commission and ending its U.S. crypto staking program as a result.

You’re reading State of Crypto, a CoinDesk newsletter looking at the intersection of cryptocurrency and government. Click here to sign up for future editions.

Banning all staking

The narrative

The U.S. Securities and Exchange Commission (SEC) announced charges against crypto exchange Kraken on Thursday, alleging its offering of a crypto staking-as-a-service program amounted to offering unregistered securities products in the U.S. To settle the charges, Kraken is paying $30 million and shutting all of its U.S. staking services. (CoinDesk was the first to report this news.)

Why it matters

The action’s raised a number of questions about what this means for staking at large in the U.S.

Before we get further into this, it’s worth defining some terms. Proof-of-stake is a consensus mechanism wherein nodes are supported by people locking up, or “staking,” their crypto. It differs from proof-of-work consensus mechanisms in that rather than putting energy and computing power into securing the blockchain, you’re putting your “money.”

Staking has gotten an increasing amount of attention in recent years, especially in 2022 after Ethereum, the world’s second-most-valuable cryptocurrency network, transitioned from proof-of-work to proof-of-stake.

Companies offer staking services in the U.S. because operating your own node just isn’t as easy as letting someone else do it for you (I’m not judging!).

Breaking it down

Coinbase CEO Brian Armstrong raised the alarm on Wednesday when he tweeted about rumors the SEC was targeting retail staking at large.

But it seems to me that what’s really happening is the SEC is going after companies like Kraken, which are offering staking services and promising their customers some kind of yield.

Let’s look at SEC Chair Gary Gensler’s own past remarks to set a bit of a baseline here: In September he said staking could meet the parameters of the Howey Test.

He highlighted intermediaries in an interview with the Wall Street Journal, saying staking through an intermediary “looks very similar – with some changes of labeling – to lending.”

Some of the big questions bouncing around after the Kraken announcement (and, to be quite frank, Armstrong’s tweet) include whether the SEC is going after all staking in the U.S., how crypto companies can actually offer staking services and whether the SEC would offer any guidance for companies hoping to offer services without drawing the agency’s ire.

An SEC official, speaking at a media briefing after the settlement’s announcement, told reporters that the agency basically looks at the offering of a staking service as being similar to offering any other type of security.

In other words, companies hoping to offer staking services would have to register as a securities platform with the regulator, get SEC Division of Corporation Finance approval to offer the product and file regular disclosures.

The security in this case was the investment program itself, meaning the representations Kraken made in offering the product and the agreement it entered into with its users, another official said.

SEC Commissioner Hester Peirce, in one of her most fiery dissents to date, pointed out that the mere act of registering may be more complex than at first glance.

“An offering like the staking service at issue here raises a whole host of complicated questions, including whether the staking program as a whole would be registered or whether each token’s staking program would be separately registered and what the accounting implications would be for Kraken,” she said.

The officials declined to comment on whether the case had any implications on staking at large.

Another component of the lawsuit the SEC filed against Kraken noted that the company determined what the staking rewards would be for users. The exchange was not just sending the actual protocol rewards to Kraken’s investors.

This may have been a big factor here. As attorney Gabe Shapiro points out, this likely “does make a big difference legally.”

An SEC official did say during the briefing the agency couldn’t comment much on this aspect, though the official did say not to read too much into it.

Stories you may have missed

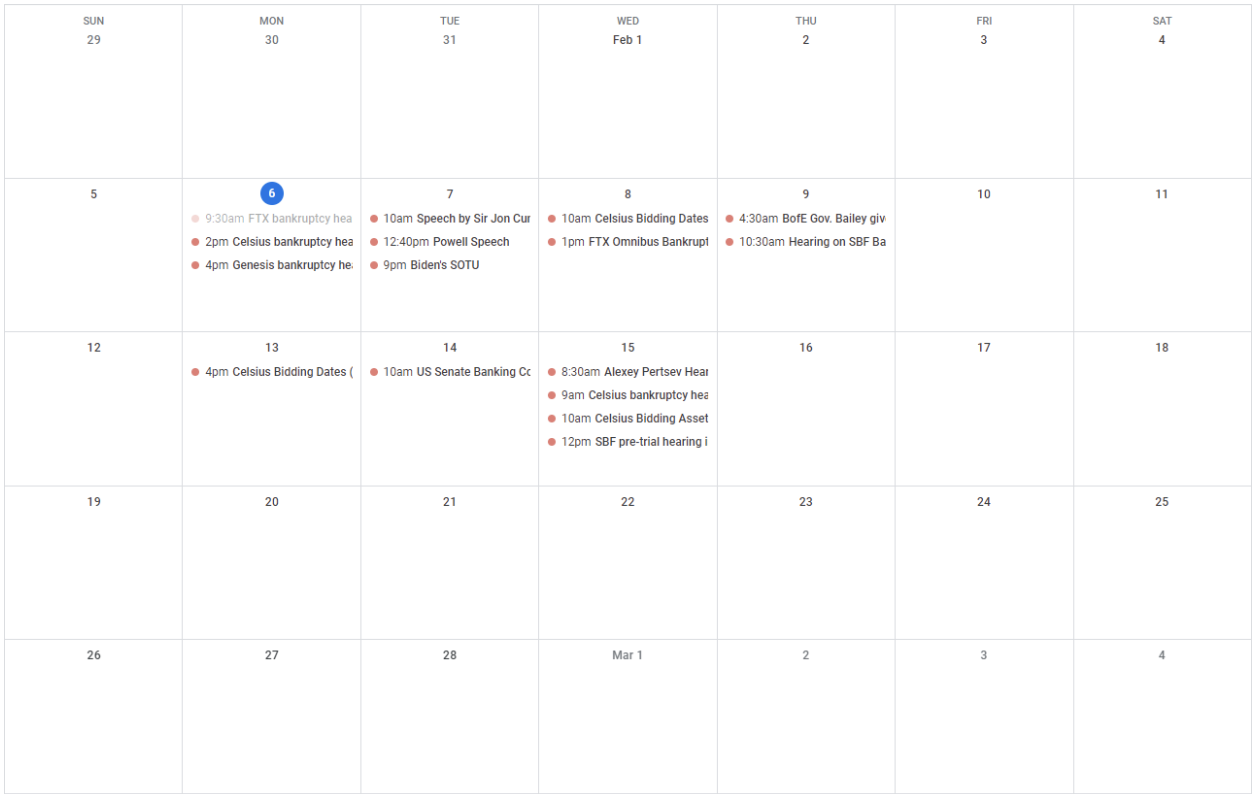

Upcoming

(CoinDesk)

Monday

Wednesday

Thursday

Elsewhere:

If you’ve got thoughts or questions on what I should discuss next week or any other feedback you’d like to share, feel free to email me at nik@coindesk.com or find me on Twitter @nikhileshde.

You can also join the group conversation on Telegram.

See ya’ll next week!